News

How To Determine Your Pricing Strategy

January 13, 2023

A common issue that many business owners face is determining how they will price their work. Many fall into the trap of charging what they think their customers will pay or mirroring what their competitors charge. However, for your business to be successful, you need to price strategically to ensure that you receive adequate compensation for your hard work and are earning a profit.

Before you price your work, you first need to understand the key figures that will impact your take home profit, which include:

- Sales revenue – The price that you charge your customers for a product or service.

- Cost of sales – The direct costs associated with the product or service, including labour, material costs, packaging, freight, GST, etc.

- Gross profit – The money left over after you subtract the cost of sales from the sales revenue.

- Overheads – Your fixed expenses that are the cost of doing business, such as rent, electricity, insurance, loan repayments, etc.

- Net profit – The final sum after subtracting overheads from gross profit.

You need to know exactly how much these expenses cost you before working out how to price your products and services. Knowing how much money you need left over to meet your profit goals after covering your expenses is essential in determining the final price that is charged to the customer.

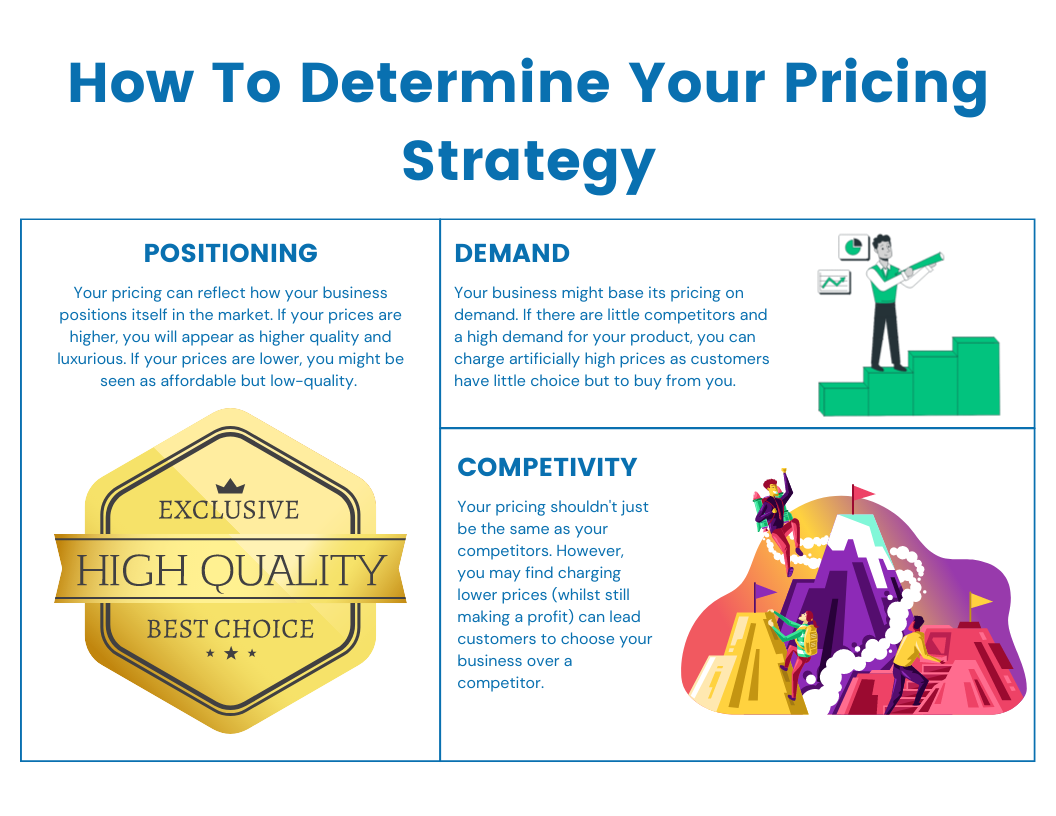

In addition to your expenses, your pricing strategy will also need to follow the marketing objectives of your business. As pricing plays a big factor on whether customers will value your business and purchase from it, your business should carefully consider how pricing will impact the following:

- Positioning – Your business’ positioning refers to how customers and competitors will view your products and services. For example, if your business charges high prices, this may indicate that your products and services are high quality and luxurious. However, if you price your items too low, people might think your business is poor quality and low status. Both have their pros and cons, so you need to determine where you want your business to fit.

- Competitivity – Whilst your business shouldn’t copy your competitors’ prices, it is important to be mindful of what they are charging and how it compares to your business. If you are charging far more for a product or service of similar quality, it is likely that you are losing a lot of customers to your competitor. However, if you are charging too little, you may be missing out on profits.

- Demand – Your business may want to alter pricing to increase demand. An example of this, may be temporarily running a sale to get new customers, and hiking prices up again once you have too many or enough customers.

Setting your pricing strategy isn’t a one-time process, you need to be reviewing this every time you submit an invoice to ensure that you are meeting your profit goals. As time goes on, your business expenses and your customers will change, so it is important to keep an eye on your strategy to stay profitable.

Acknowledgement Of Country

Business Foundations acknowledges the traditional custodians throughout Western Australia and their continuing connection to the land, waters and community. We pay our respects to all members of the Aboriginal communities and their cultures; and to Elders both past and present.

Victoria

The Commons

80 Market Street,

South Melbourne VIC 3205

admin@businessfoundations.com.au

Western Australia

Wesley Central

2 Cantonment Street,

Fremantle WA 6160

admin@businessfoundations.com.au

Get In Touch

Have a question or to find out how we can help you, please get in touch.